The memecoin launchpad Pumpfun, which launched in January 2024, has rapidly established itself as a major player in the cryptocurrency space.

In less than two years, it has transformed the way people launch and trade tokens enabling even complete beginners to create tradable digital assets in minutes.

This meteoric rise has not only captured global attention but also attracted the scrutiny of regulators and tax authorities. As the platform continues to grow, questions are mounting over how its operations align with existing laws, especially in jurisdictions where digital asset frameworks are still evolving.

This article covers the legal aspects of Pumpfun from both U.S. and EU perspectives, with a particular focus on the Markets in Crypto-Assets (MiCA) regulation. It also highlights some potential tax implications for both token creators and investors navigating the memecoin economy.

What is Pumpfun?

Pumpfun is a platform that allows anyone — even those without technical skills — to create and trade tokens within minutes. Every token on Pumpfun is a fair launch, meaning all participants have the same opportunity to buy and sell from the start.

Key features that set Pumpfun apart include:

▪︎ Low fees

▪︎ Fair launch system

▪︎ No technical barrier

▪︎ Speed of deployment

▪︎ A bonding curve model

▪︎ A user-friendly interface

▪︎ An engaged community

Platform Growth and Milestones

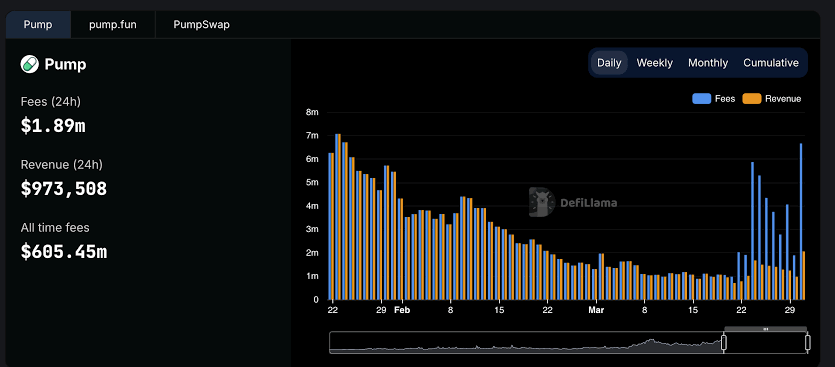

By mid-2025, Pumpfun had launched millions of tokens, expanded to the Base and Blast networks, and raised an astonishing $500 million in under 12 minutes during its $PUMP token ICO on July 12, 2025. On peak days, the platform accounted for over 70% of new Solana token launches, with weekly trading volumes reaching $2.2 billion.

Unsurprisingly, this explosive growth has drawn heightened legal scrutiny in both the United States and the European Union, alongside increasing tax compliance obligations.

The recent $PUMP ICO also demonstrated that, beyond Bitcoin, Ether, and established altcoins, investors are eager to participate in memecoins and other emerging crypto projects.

The Bonding Curve Model and Market Dynamics

A central aspect of Pumpfun’s popularity is its use of the bonding curve model. It is a mathematical framework in cryptocurrency and DeFi that links a token’s price to its supply. Under this model, as supply increases, price rises according to a predefined formula (and vice versa).

This approach can help regulate token distribution, liquidity, and even governance.

However, despite the advantages of this model, Pumpfun’s $PUMP token saw a sharp drop in market value post-ICO — from a $4 billion fully diluted valuation (FDV) to below $2 billion FDV.

This decline may be partly attributed to a delayed airdrop announcement by the co-founder, but it also raises concerns about potential pump-and-dump schemes.

A pump-and-dump scheme is a form of market manipulation common in both traditional finance and cryptocurrency markets.

It involves artificially inflating the price of a low-value token or asset through misleading hype and promotion, attracting unsuspecting investors driven by fear of missing out (FOMO).

Once the price rises to a profitable level, the token creators sell off their holdings, causing the price to crash and leaving late buyers with significant losses.

This fraudulent tactic typically progresses through phases of pre-launch hype, launch promotion, price pump, and final dump

Legal Landscape in the United States.

Pumpfun faces multiple legal challenges in the U.S., primarily through class-action lawsuits filed since January 2025.

A prominent lawsuit, filed by Diego Aguilar on January 30, 2025, in the U.S. District Court for the Southern District of New York, accuses Pumpfun, its operator Baton Corporation Limited, and co-founders Alon Cohen, Dylan Kerler, and Noah Bernhard Hugo Tweedale of orchestrating a $500 million pump-and-dump scheme.

The suit alleges that tokens like FRED, FWOG, and GRIFFAIN were promoted as unregistered securities, lacking investor protections such as Know Your Customer (KYC) and anti-money laundering (AML) protocols. These tokens are claimed to meet the Howey Test criteria for securities due to reliance on Pumpfun’s marketing and infrastructure.

A separate lawsuit, filed by Kendall Carnahan on January 16, 2025, targets the PNUT token, which surged to a $1 billion market cap before crashing, resulting in significant investor losses.

In addition, a July 2025 Racketeer Influenced and Corrupt Organizations Act (RICO) lawsuit alleges that Pumpfun, alongside Solana’s co-founders, operated a “Meme Coin Casino” using “dark money” to coordinate Maximum Extractable Value (MEV) bot extractions, potentially manipulating token launches, according to some information available on X (Twitter).

While these allegations remain unverified, they highlight concerns over market manipulation and inadequate investor protections.

U.S. Regulatory Context

At the moment, there’s no unified crypto regulatory framework in the States, with the SEC and Commodity Futures Trading Commission (CFTC) both applying existing laws. There’s a SEC staff statement that mentions that “true” memecoins—those created for entertainment without investment contract features—may not be securities.

However, tokens promoted with profit expectations, like those on Pumpfun, risk classification as securities under the Howey Test, requiring registration under the Securities Act of 1933 and the Securities Exchange Act of 1934.

The mere fact that the $PUMP token during its ICO has not been allowed for purchase for U.S. users is an example of the still-present uncertainties in regard to the memecoins around the globe, especially in the USA. Another point of view to be considered is the GENIUS Act.

While not directly targeting memecoins, it signals a broader regulatory tightening that could impact Pumpfun if its tokens are deemed securities or if it is classified as a broker under SEC rules.

Legal Landscape in the European Union (MiCA)

The EU’s MiCA regulation, fully effective as of December 30, 2024, provides a harmonized framework for crypto-assets, more specifically, e-money tokens (EMTs), asset-referenced tokens (ARTs), or other crypto assets. Memecoins likely fall into the “other” category, requiring issuers to publish a whitepaper detailing risks, technical roadmaps, and compliance measures, all in accordance with the regulation and the following subsidiary acts.

Key MiCA requirements for Pumpfun include, but might not be limited to:

- Whitepaper Obligations:

Token issuers, potentially including Pumpfun as a co-issuer due to its automated tools, must comply with whitepaper requirements.

Some of these are aimed towards providing detailed information regarding the token, its issuers, team, purpose, etc. Another specificity of this regime is the provisioning of information regarding potential risks such as value loss, restricted transferability, illiquidity, and the potential inability to exchange the tokens for promised goods or services. A set of disclaimers shall also be present in order for the whitepaper to be considered compliant.

Market Integrity Rules:

MiCA prohibits market manipulation, such as pump-and-dump schemes, with ESMA and national regulators enforcing compliance through transaction monitoring. These requirements apply to all participants from the moment of entering into force of the regulation, regardless of the grandfathering period in some jurisdictions.

■ Other legal acts in the EU

MiCA aligns with the EU’s Anti-Money Laundering Directive (AMLD5). Pumpfun’s reported lack of KYC/AML checks, as alleged in U.S. lawsuits, could attract EU scrutiny if it facilitates illicit activities. Furthermore,

The EU’s Digital Services Act (DSA) investigations into X (previously Twitter) for deceptive practices may indirectly impact Pumpfun’s marketing, given its reliance on social media hype.

Tax Implications for Pumpfun Users and Operators

■ U.S. Tax Perspective

The IRS classifies cryptocurrencies, including memecoins, as property, making every transaction a taxable event. Implications for Pumpfun users include:

- Capital Gains/Losses: Selling memecoins triggers capital gains tax—short-term (held ≤ 1 year) at ordinary income rates or long-term (held > 1 year) at preferential rates. Losses can offset gains, necessitating detailed records.

- Ordinary Income: Airdrops or incentives, such as $PUMP tokens, are taxed as ordinary income at their fair market value upon receipt.

- Form 1099-DA Reporting: From January 1, 2025, crypto brokers (potentially including Pumpfun) must report gross proceeds to the IRS via Form 1099-DA, with cost basis reporting required by January 1, 2026, increasing IRS visibility.

■ EU Tax Perspective

Taxation in the EU varies by member state, as it remains a national competence. General principles and upcoming regulations include:

- Income and Capital Gains Tax: Memecoin trading profits are subject to income or capital gains tax, with variations (e.g., Germany taxes gains after a one-year holding period for private investors; France applies a flat rate for frequent traders).

- VAT Considerations: Fiat-to-crypto exchanges are typically VAT-exempt, but platform services like Pumpfun’s bonding curve may incur VAT, depending on the jurisdiction.

- DAC8 Reporting: Effective January 1, 2026, DAC8 (Directive on Administrative Cooperation (tax transparency for crypto-assets) requires CASPs to report EU clients’ crypto transactions to national tax authorities, with data exchanged across member states.

Conclusion

Pumpfun’s ICO shows just how complex the crypto world can be. On one hand, it was a huge success; on the other, it raised serious concerns.

In the U.S., ongoing lawsuits and unclear regulations threaten its operations, while in the EU, MiCA rules bring strict compliance requirements.

From a tax standpoint, anyone buying $PUMP or other memecoins should remember that these purchases may be taxable or require reporting to authorities through the relevant CASP.

And finally, one of the most important pieces of advice in both crypto and finance: DYOR — Do Your Own Research!

References

[1] Pump.fun Board — https://pump.fun/board

[2] CryptoSlate, Pump.fun hit with federal lawsuit… — https://cryptoslate.com/pumpfun-hit-with-federal-lawsuit-over-alleged-500m-pump-and-dump-scheme/

[3] Coinbase, What is a pump and dump in crypto?

[4] CryptoSlate (same as [2])

[5] The Howey Test — Investment contract criteria under U.S. securities law

[6] Howey Test Definition: Implications for Cryptocurrency

[7] MiCA Regulation (EU 2023/1114) — EUR-Lex

[8] AML Directive (EU 2018/843) — EUR-Lex

[9] IRS, Digital Assets — https://www.irs.gov/digital-assets

[10] European Commission, DAC8 — Directive on Administrative Cooperation

.jpg)

.jpg)

.png)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.JPEG)

%20(1).jpg)

.png)

.jpg)

.jpg)

.jpg)

.png)

.png)

.png)

.jpeg)

.jpg)