- On 18 March 2026, the European Commission proposed EU Inc., an optional single company framework across the EU.

- Founders can set up a company online in 48 hours for under €100, with no minimum capital.

- A new EU stock option plan delays taxes until shares are sold.

- Tax rules still differ by country, so companies face complexity across borders.

- The new framework simplifies company setup, but tax differences remain the bigger challenge.

Introduction

On 18 March 2026, the European Commission unveiled what might be the most ambitious attempt to reshape how businesses operate across the continent. The proposal, called EU Inc., introduces a single, optional corporate framework that lets any entrepreneur register a company in 48 hours, fully online, for less than 100 euros. It is the centrepiece of what Brussels calls the “28th regime”, a unified set of rules that sits alongside the 27 existing national legal systems rather than replacing them.

The ambition is clear. The execution raises questions. Because while company law is getting harmonised, tax systems across Europe remain firmly national. And for any founder trying to scale across borders, tax is where the real complexity lives.

What the 28th Regime Actually Does

To understand why this proposal matters, consider what European founders deal with today. The EU has 27 national legal systems and more than 60 different company forms. Setting up in one country can take weeks. Expanding into a second means hiring local lawyers, navigating a separate registration process, and adapting to an entirely different set of corporate rules. The Commission's own public consultation found that over 80% of respondents considered these divergent rules a significant obstacle to starting or running a business in the EU.

EU Inc. is designed to cut through this. A founder in Lisbon, Tallinn, or Amsterdam can register a single legal entity that operates under one set of corporate rules across all 27 member states.

Key features of EU Inc.:

- No minimum capital required, so founders can start a company without upfront funds

- Fully online registration in under 48 hours for less than €100

- Company data is submitted once and shared automatically with tax, VAT, and social security systems

- A single EU stock option framework where employees are taxed only when shares are sold

- Flexible share structures with different rights for different investors

- Digital share transfers without the need for a notary

- Simpler insolvency rules that make it faster and cheaper to close a failed startup

- Option for companies to access public markets, depending on the member state

As European Commissioner Michael McGrath put it when presenting the proposal:

''Europe has talent, ideas and ambition but bureaucracy has been driving its best entrepreneurs elsewhere''

The Gap Proposal Leaves Open: Tax

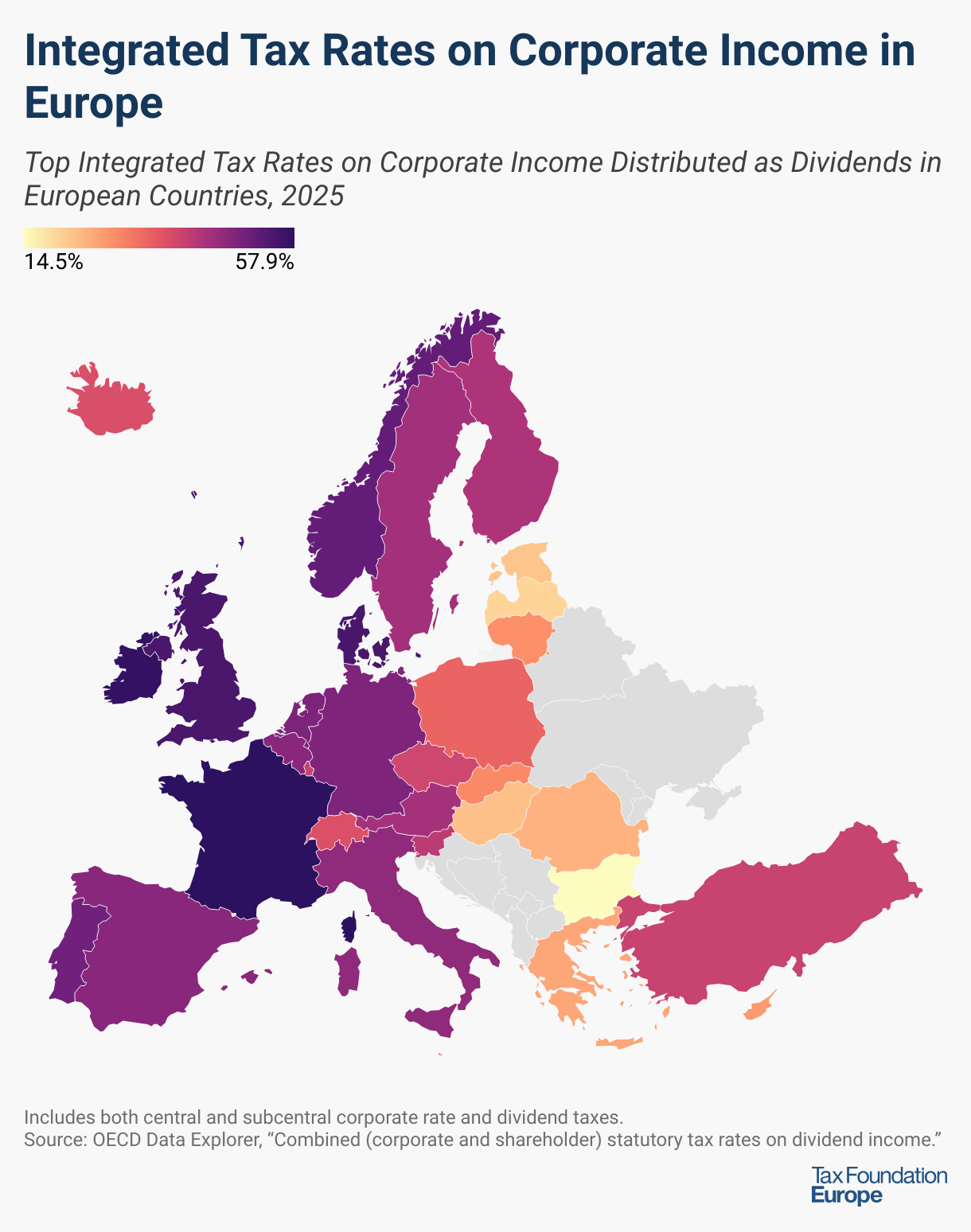

This is where things become more complex. Tax obligations remain governed by national systems. While a company may operate under a single legal framework, its tax position is still determined by where it is resident, where value is created, and where its activities take place.

In practice, this means dealing with multiple tax regimes at once. Corporate tax rates differ across member states. Transfer pricing rules apply when operations span jurisdictions. Reporting obligations, VAT registration, and local compliance requirements do not disappear under a unified company framework.

Is tax harmonisation even possible across all 27 member states? Politically, it remains one of the most difficult areas to align.

The European Commission has acknowledged this gap. Alongside the 28th regime, it points to complementary initiatives such as the Head Office Tax System (HOT) for SMEs and the Business in Europe: Framework for Income Taxation (BEFIT). Both aim to simplify certain aspects of corporate taxation, but neither replaces national tax sovereignty.

This matters because for founders and investors, the complexity does not disappear. It shifts. A company may be incorporated once, but it is still taxed in multiple places. In practice, this is where the real challenges begin.

Why This Matters for Startups and Scale-Ups

The conversation around the 28th regime is not just about incorporation. It is about whether Europe can create companies that scale.

One issue that repeatedly comes up is the so-called “dry income” problem. In many EU countries, employees are taxed on stock options when they are granted, not when they are sold. This creates a situation where employees may owe tax on value they have not realised, and may never realise if the company fails. For early-stage companies, this makes equity-based compensation far less attractive compared to jurisdictions like the United States.

Fragmentation also creates practical barriers. A company operating across multiple EU countries often needs separate employee stock option plans, each aligned with local tax rules. The administrative cost alone can be prohibitive.

Tax incentives, where they exist, are often too complex or inaccessible for startups. Pre-revenue companies may not benefit from credits they cannot use, and smaller firms may lack the resources to navigate complex systems.

Taken together, these issues do not stop companies from starting. They stop them from scaling efficiently.

What the 28th Regime Changes in Practice

For founders and early-stage companies, the EU Inc. proposal represents a genuine step forward. Registering a pan-European entity in 48 hours for 100 euros with no minimum capital requirement removes friction that has historically pushed ambitious founders to leave the EU. The harmonised stock option framework addresses one of the most persistent pain points in European startup hiring. And the simplified insolvency procedures reduce the cost of failure, making it easier for entrepreneurs to try again.

The 28th regime represents a meaningful step toward reducing legal fragmentation. Incorporation becomes faster. Administrative processes become simpler. Founders can operate under a single corporate framework across the EU. But beyond that initial step, the reality remains largely unchanged.

But the proposal is a starting point, and its architects acknowledge this. As the Draghi Report diagnosed, legal fragmentation across the single market functions as an invisible tariff on cross-border growth. EU Inc. lowers that tariff for company law. It does not lower it for taxation.

A company will still need to assess where it is tax resident. It will still need to comply with local tax rules in each jurisdiction where it operates. It will still face different treatments of income, incentives, and reporting obligations. The result is a system where the legal layer is simplified, but the tax layer remains complex.

This reflects a broader design choice behind the 28th regime. Policy discussions around the proposal have been clear that it focuses primarily on corporate law, while deliberately avoiding more politically sensitive areas such as tax. While this makes the proposal more feasible, it also limits how much of the overall complexity it can realistically remove.

For some companies, this may still be a significant improvement. Reducing legal friction at the start can make cross-border expansion more accessible. But for others, especially those scaling quickly across multiple jurisdictions, tax will continue to define the real level of complexity.

The Bottom Line

The 28th regime addresses a real and well documented problem. Legal fragmentation has long made it harder to build and scale companies across Europe. But it does not address the full picture. As long as tax systems remain national, a single company framework can only go so far. The EU is simplifying how companies are formed. It has not yet simplified how they are taxed. For founders, investors, and operators, that distinction matters.

The question is no longer whether the 28th regime makes things easier. It is whether it goes far enough to change how companies actually scale in Europe.

If you are working across jurisdictions or planning to, now is the time to get ahead of the tax implications. Speak with our team for tailored guidance, stay informed by subscribing to the newsletter, and join the discussion at the Crypto Tax Forum.

.jpg)

.jpg)

.png)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.JPEG)

%20(1).jpg)

.png)

.jpg)

.jpg)

.jpg)

.png)

.png)

.png)

.jpeg)

.jpg)