.png)

- Crypto is now fully transparent globally. Under OECD CARF, transaction data will be automatically shared between countries starting in 2027, so relocating no longer hides activity.

- The 183 day rule is not enough. Tax residency depends on overall life connections like home, family, and finances, and getting it wrong can lead to double taxation.

- US citizens face extra complexity. The US taxes worldwide income, and leaving the system can trigger an exit tax on unrealized crypto gains.

- Tax friendly destinations still exist. The UAE, Portugal, and Germany offer advantages, but each comes with strict conditions and trade offs.

- Execution is critical. Weak planning, lingering ties to your home country, or missing FBAR and FATCA obligations can result in severe penalties.

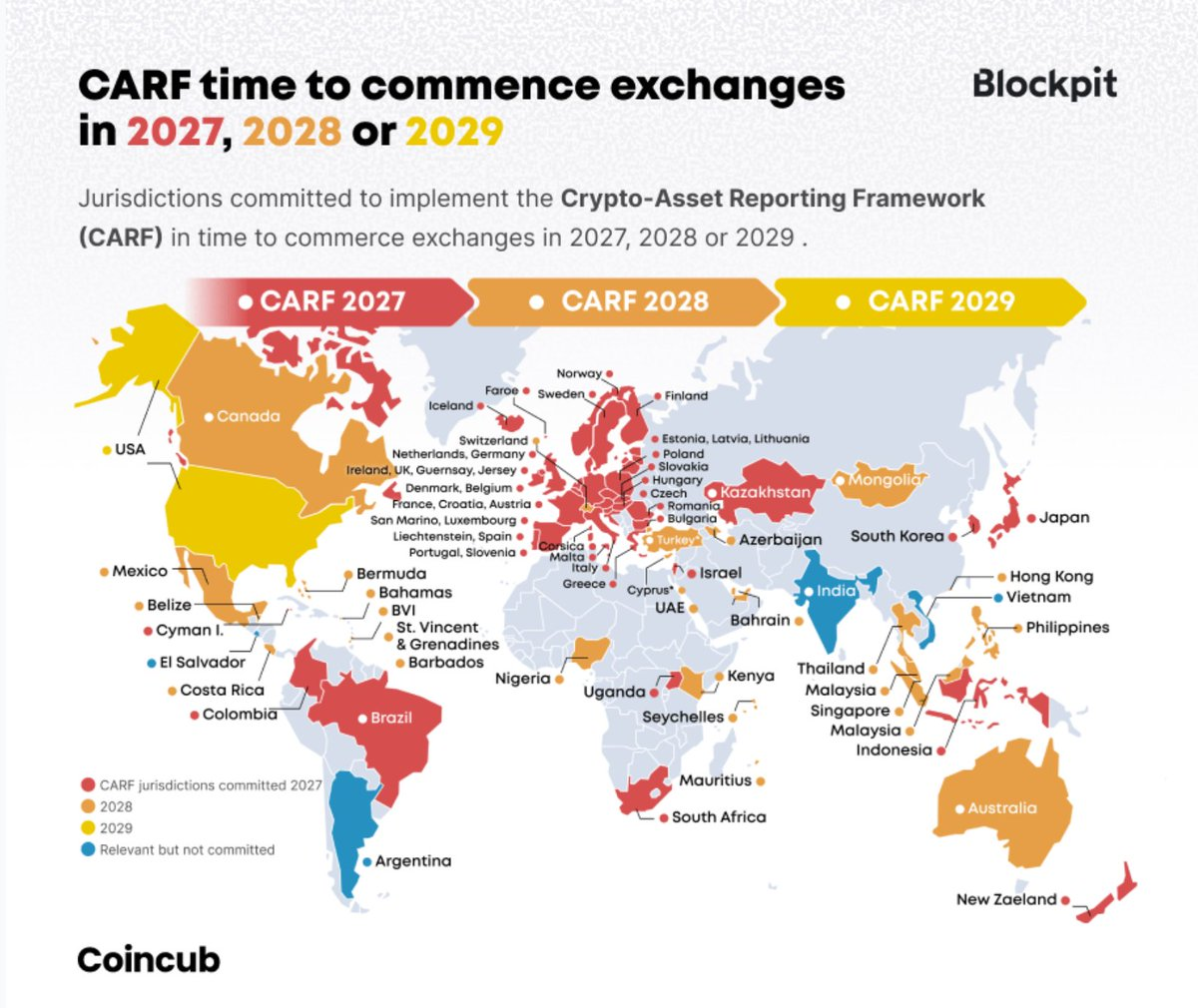

Crypto tax relocation is no longer as simple as booking a one-way flight. With the first 47 jurisdictions already collecting your crypto transaction data under the OECD’s new reporting framework, and 76 committed in total with automatic sharing set to begin in 2027, getting this wrong could cost you hundreds of thousands of dollars.

Here's what you need to know before making the move.

How CARF 2026 Changed Crypto Tax Reporting Worldwide

The OECD's Crypto-Asset Reporting Framework (CARF) took effect on January 1, 2026. Crypto exchanges and wallet providers across the first group of jurisdictions began collecting transaction data on that date and will automatically report it to tax authorities starting in 2027.

A second group, including Australia, Hong Kong, Singapore, Switzerland, and the UAE, will join in 2028. The United States is not participating in CARF but maintains its own reporting regime under FATCA. Over 76 jurisdictions have committed, with the first wave beginning data collection in 2026.

What gets reported?

- Your name

- Address

- Tax identification number

- Transaction records

- Year-end balances

While wallet address reporting was narrowed in the final rules, transaction-level transparency remains extensive.

Tax authorities will share this data automatically with your country of tax residence. Simply moving abroad no longer erases your obligations at home. You must properly establish new tax residency or risk being taxed in both countries.

The 183-Day Myth of Crypto Tax Relocation

One of the most persistent myths among crypto holders considering relocation is the "183-day rule," which is the idea that spending 183 days in a new country automatically makes you a tax resident there and frees you from obligations elsewhere. It doesn't.

Tax residency is determined by a range of factors beyond physical presence. Authorities examine where you maintain a permanent home, where your family lives, your business and banking ties, and even where you vote. You could spend 200 days in Lisbon and still be treated as a US tax resident if your spouse, children, home, and primary business interests remain stateside.

The result is taxation in both countries, penalties, and costly legal disputes, precisely the outcome relocation was meant to avoid.

The US Exit Tax: A Particular Problem for Crypto Holders

The United States taxes its citizens on worldwide income regardless of where they reside. Moving to Dubai or Lisbon changes nothing about your federal obligations, which makes the US a uniquely difficult jurisdiction to leave.

The only path out is expatriation; this means renouncing citizenship or abandoning a long-term green card. This triggers the exit tax under IRC Section 877A, which treats you as having sold all assets the day before expatriation.

You qualify as a "covered expatriate" and owe the exit tax if you meet any of three thresholds. The most recently confirmed figures (for 2025) are: a net worth exceeding $2 million, an average annual net income tax liability above $206,000 over the past five years, or failure to certify five years of tax compliance. Official 2026 thresholds have not yet been published, but are expected to increase modestly with inflation.

The 2025 one-time exclusion was $890,000.

To illustrate:

If you purchased Bitcoin in 2017 for $50,000 and your crypto portfolio is now worth $3.2 million, your gain of $3,150,000 minus the exclusion leaves $2,260,000 in taxable gains. At the 20% long-term capital gains rate plus the 3.8% Net Investment Income Tax, the federal exit tax alone comes to roughly $537,880. Add California's 13.3% state tax and the total climbs substantially higher.

The Roger Ver Case

The case of Roger Ver, known in crypto circles as 'Bitcoin Jesus,' shows what happens when expatriation goes wrong. Ver renounced his US citizenship in 2014 after obtaining citizenship in St. Kitts and Nevis. He held approximately 131,000 Bitcoin, worth roughly $73.7 million at the time, but allegedly failed to properly report those holdings to his tax preparers during the expatriation process.

The IRS used blockchain analysis to trace his assets. Ver was indicted in 2024, but in October, 2025 reached a deferred prosecution agreement with the DOJ, paying nearly $50 million in back taxes, penalties, and interest. The indictment was dismissed, but the lesson is clear. The IRS has the tools to follow crypto across borders, and concealment is not a viable strategy.

That reality sets the stage for the next question: If you are going to relocate, where should you go?

Where to Relocate: Three Crypto-Friendly Destinations in 2026

CARF has narrowed the field, but legitimate opportunities remain. The image below offers a comparative snapshot of how EU countries approach the taxation of crypto gains, highlighting the trade-offs between different regimes.

With that broader picture in mind, three destinations stand out as particularly worth your attention:

1. Portugal

Portugal introduced a 28% tax on short-term crypto gains in 2023, ending its era as a pure crypto haven. Under the current rules, crypto held for under 12 months faces a 28% tax; holdings beyond that threshold are tax-free.

Crypto-to-crypto swaps are tax-deferred, not permanently exempt, and the swap resets the 365-day holding period for the new asset. NFTs are currently not explicitly taxed in many cases, but treatment depends on facts and classification.

Residency options include the D7 visa, requiring approximately €10,440 per year (€870/month) in passive income, or the Golden Visa, which now requires a €250,000 investment in artistic production or cultural heritage (the real estate pathway has been eliminated).

In October 2025, Portugal's parliament approved legislation extending the residency requirement for citizenship from five to ten years. After a Constitutional Court ruling and presidential veto, a revised version was re-approved in April 2026, but is not yet in force. Portugal joins CARF exchanges in 2027.

2. United Arab Emirates

The UAE offers the most straightforward zero-tax regime. There is no personal income tax, capital gains tax, or wealth tax on crypto holdings. Businesses operating in the crypto space may face a 9% corporate tax, and VAT of 5% applies to goods and services, but not to crypto trading itself.

The Golden Visa requires an AED 2 million (~$545,000) real estate purchase or qualification as an entrepreneur or specialized talent. Tax residency can be established through several tests, including physical presence thresholds and economic ties. The cost of living in Dubai and Abu Dhabi is significant. The UAE joins CARF in 2028.

3. Germany

Germany is often perceived as a “tax-free” jurisdiction for long-term crypto holders, but this characterization is overly simplistic.

The 12-month holding rule, which allows for tax-free capital gains, applies only within the scope of private asset management. Where activities such as staking, lending, or more frequent trading are undertaken, this can alter the classification of the assets and potentially invalidate the exemption.

In such cases, gains may become fully taxable, particularly if the activity is deemed to constitute a commercial or business operation.

Three Mistakes That Trigger Double Taxation

Even with the right destination, certain errors consistently lead to the most expensive outcomes.

a. Maintaining ties to your departure country: Keeping your home, bank accounts, and family in the country you claim to have left invites tax authorities to argue that you never truly relocated. Substance matters more than paperwork.

b. Ignoring reporting obligations separate from tax filings: US citizens, for instance, must file an FBAR for foreign accounts exceeding $10,000. Willful failure to file carries a penalty of up to 50% of the account balance per year. FATCA imposes further requirements for foreign assets exceeding $50,000 to $200,000, depending on filing status. Even if you pay every dollar of tax owed, missing these filings triggers severe penalties.

c. Assuming crypto is invisible: Tax authorities around the world use blockchain analytics platforms such as Chainalysis and Elliptic to trace transactions. Combined with CARF's automatic exchange reporting, the era of undetected crypto holdings is over.

A Practical Relocation Checklist

a. Six to twelve months before moving:

- Inventory all crypto holdings and calculate unrealized gains.

- Engage cross-border tax professionals with experience in both your departure and destination jurisdictions.

- Review your complete financial picture: bank accounts, real estate, business interests and choose your destination based on quality of life and genuine intent, not tax rates alone.

b. During the move:

- Document everything meticulously: location records, utility bills, rental agreements, travel itineraries.

- File the required departure forms (Form 8854 for US expatriates).

- Establish genuine local presence: open bank accounts, obtain a driver's license, register with local authorities, and engage with the community.

- Update your address on all crypto platforms and ensure you meet physical presence requirements.

c. After the move:

- File tax returns in both jurisdictions as required.

- Maintain robust documentation proving genuine residence.

- Report foreign accounts under FBAR, FATCA, and destination country rules.

- Monitor compliance closely, particularly as CARF reporting begins in 2027 for the first group of jurisdictions.

- Re-evaluate your situation annually.

Crypto tax laws evolve rapidly, and what works today may not hold up next year.

The Bottom Line

Crypto tax relocation in 2026 is not about finding loopholes; it is about making a genuine life change that happens to carry legitimate tax benefits. CARF, blockchain analytics, and deepening international cooperation have made transparency mandatory, not optional. The digital nomad strategy of maintaining no fixed tax residence while moving between countries is increasingly untenable.

For many holders, domestic strategies may be more practical: tax-loss harvesting, holding assets for long-term capital gains treatment, maximizing retirement account contributions, or donating appreciated crypto to charity. But for those with significant portfolios and a genuine willingness to build a life abroad, the savings can be substantial, provided the process is handled with professional guidance and rigorous compliance.

The worst outcome is the half-measure: relocating on paper while your real life stays behind, then facing taxation and penalties in both jurisdictions.

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.JPEG)

.png)

.jpg)

.jpg)

.jpg)

.png)

.png)

.png)

.jpeg)

.jpg)